The average loan officer spends 37% of their workday on administrative tasks that don’t require a mortgage license. According to STRATMOR Group’s 2025 Origination Performance Study, brokers who delegate administrative work to a dedicated support role close 2.3x more loans annually than those who handle everything themselves. The math isn’t complicated. The execution is where most brokers fall short.

This isn’t a feature roundup. Every CRM vendor publishes that. This is a guide to what a trained mortgage virtual assistant actually does inside each platform to keep your pipeline moving from application to clear-to-close, without your hands on every task.

The Real Problem Isn’t the Software

The Mortgage Bankers Association reported that the average cost to originate a loan hit $12,593 in 2024, up from $9,470 in 2021. That number keeps climbing because loan officers bury themselves in work that an unlicensed support person could handle: status update calls, condition reminders, document follow-ups, pipeline reports, and Realtor partner updates. When your highest-cost producer spends Tuesday afternoon chasing a missing W-2, you’ve paid a licensed professional’s hourly rate for a filing task.

A well-configured CRM with a trained VA running day-to-day operations shifts that ratio fast. But the CRM alone changes nothing. It’s a tool. It produces results when someone takes ownership of the system and works it every single day.

STRATMOR’s 2025 data shows loan officers with dedicated administrative support averaged 8.4 loans closed per month, compared to 4.1 for those working alone. That’s not a marginal edge. That’s the difference between a business that scales and a grind that wears through producers.

What Your VA Can and Cannot Do

This needs to be clear before we discuss any specific platform, because it protects your license and your clients.

The SAFE Act of 2008 requires anyone who takes a mortgage application, offers or negotiates loan terms, or provides loan guidance to hold an active NMLS license. Your VA holds no such license. The GLBA (Gramm-Leach-Bliley Act) governs how non-licensed staff interact with borrower data, and TRID (TILA-RESPA Integrated Disclosure) adds precise disclosure timeline requirements that shape what your VA tracks versus what you sign off on.

Here’s the line in plain terms:

VA Scope of Work: Quick Compliance Reference

| What They CANNOT Do (SAFE Act) | What They CAN Do (GLBA-Compliant) |

|---|---|

| Discuss interest rates with borrowers | 1003 data entry and cross-referencing |

| Quote origination fees or closing costs | Document condition collection via Floify |

| Advise on loan products or programs | Milestone status updates to all parties |

| Interpret or explain disclosure documents | TRID timeline tracking and audit logs |

| Negotiate terms on behalf of the broker | Realtor pipeline reports and partner updates |

| Access pricing engines or rate sheets | CRM database hygiene and contact management |

Every CRM on this list supports role-based access controls. Configuring those correctly is step one before your VA logs in for the first time. It takes less than an hour and protects you from an NMLS audit finding.

Total Expert: The Enterprise Standard That Most Guides Skip

Total Expert has become the dominant CRM for mid-to-large mortgage operations, with more than 200,000 financial services professionals on the platform as of 2025. Enterprise lenders including Fairway Independent Mortgage and CrossCountry Mortgage run their referral management and compliance workflows through it. If you’re building toward a high-volume operation or managing a team of five or more producers, Total Expert is the platform worth understanding first, which makes it notable that most “best mortgage CRM” guides don’t cover it.

What it does well for remote teams.

Total Expert integrates directly with Encompass, ICE Mortgage Technology’s loan origination system and the LOS that dominates the independent broker market. That integration means borrower data flows from the 1003 application into the CRM automatically, triggering milestone-based communication sequences without manual re-entry. It connects to Calyx Point and MeridianLink as well, which matters when you’re working with credit union partners or state housing programs running different origination infrastructure.

The platform’s Customer Intelligence engine is where it genuinely separates itself from smaller platforms. It monitors rate-lock expiration windows, flags equity triggers when a borrower’s home value rises enough to eliminate MIP (Mortgage Insurance Premium) payments, fires refinance prompts when prevailing rates drop below the borrower’s current note rate, and sends ARM adjustment alerts when a variable-rate borrower’s reset window approaches. These aren’t passive alerts. They’re revenue events, and each one requires someone to act on the trigger before a competitor does.

The Depth Problem: Why Total Expert Runs on Autopilot for Most Brokers

Total Expert’s depth is an asset when someone actively manages it and a liability when it runs unsupervised. Pipeline health degrades fast when contact records go stale, sequences run without response tracking, and referral partner profiles don’t get updated. Most brokers configure it once, push a few campaigns, and watch the data quality erode within 90 days. The tool gets blamed. The actual problem is the absence of consistent ownership.

How an Aristo mortgage VA executes inside Total Expert

A trained mortgage broker virtual assistant running Total Expert handles the SOP-driven tasks that keep the platform current and the Customer Intelligence engine producing real results. That means a daily review of the pipeline dashboard to flag files sitting in the same stage for more than 48 hours, updating milestone records when the LOS pushes a status change, and running the weekly referral partner update sequence so every active Realtor knows where their clients stand.

The VA manages contact hygiene: merging duplicates, updating employment and address records from 1003 data, and archiving closed files correctly. For the equity trigger and MIP drop-off alerts, the VA runs the event response workflow: confirming the trigger fired for the correct contact, queuing the outreach task for the broker at the right time, and logging the outreach so the audit trail stays clean under NMLS record-keeping standards. None of this requires a license. All of it consumes 2 to 3 hours a day that the producing broker recovers entirely.hen it drives behavior through process design.

Jungo: High-Volume Pipeline Management Built on Salesforce

Jungo runs on Salesforce’s infrastructure, which gives it enterprise-grade API connectivity and customization depth that scales with complex teams. Its core positioning targets mortgage brokers who need robust lead attribution and reporting across multiple loan officers, lead sources, and referral channels.

LOS integration and compliance capabilities

Jungo connects to Calyx Point and MeridianLink for data sync and integrates with Floify for condition collection and borrower-facing task management. Its compliance module supports NMLS record-keeping and flags disclosure timeline gaps tied to TRID, which requires lenders to deliver specific disclosures within three business days of application receipt. Missing those windows creates regulatory exposure that an NMLS audit will find.

The Salesforce Tax: Why Solo Brokers Struggle with Jungo

Salesforce’s underlying architecture means Jungo isn’t a platform you configure once and leave. It demands active management of workflows, field mapping, and user permissions as your business changes. A solo broker without Salesforce administration experience ends up with a powerful system running at 30% of its potential because pipeline stages don’t match the actual LOS milestones, automations fire on stale triggers, and reports surface the wrong data. The solo broker pays the full cost of a Salesforce-grade platform and captures a fraction of the value because nobody owns it.

How an Aristo mortgage VA executes inside Jungo

The VA’s primary role centers on data integrity and pipeline reporting. After a new 1003 gets submitted, the VA enters borrower data into the appropriate Jungo record, cross-referencing the LOS entry to catch field inconsistencies, assigns the file to the correct pipeline stage, and activates the disclosure tracking sequence. For active files, the VA runs the morning condition chase: reviewing the Floify portal for outstanding items, updating the conditions count in Jungo, and sending templated status updates to the processing team, the Realtor, and the borrower.

One Aristo client, a solo broker closing six loans per month, assigned a VA to own condition follow-up and pipeline updates inside Jungo. Time to first contact on new leads dropped from four hours to under 20 minutes. Within 90 days, monthly closings reached nine without adding local staff or changing the CRM configuration.

On the reporting side, the VA pulls the weekly pipeline report and flags anomalies: files with no activity in 72 hours, leads stuck at application stage past 14 days, and referral sources with declining conversion rates. The broker reviews a one-page summary instead of digging through records manually every Friday afternoon.

BNTouch: Multi-Channel Marketing for Active Referral Networks

BNTouch positions itself as the mortgage CRM built for loan officers who prioritize lead nurture and referral marketing over pipeline management. Its core strength is multi-channel communication: email, SMS, and direct mail campaigns that run on borrower lifecycle triggers, anniversary dates, and market condition changes.

Integration depth and compliance features

BNTouch syncs with most major LOS platforms and connects to lead sources including Zillow, Realtor.com, and LendingTree. Its SMS compliance features handle opt-in tracking, which matters under TCPA (Telephone Consumer Protection Act) rules governing text message marketing in financial services. A compliance failure on SMS marketing can generate $500 to $1,500 per message in regulatory penalties. Most solo brokers don’t realize they carry that exposure until they receive a demand letter.

The Tagging Trap: Where Self-Managed BNTouch Systems Fail

BNTouch’s marketing power depends entirely on clean contact segmentation. When contact records don’t carry correct tags for lead source, loan type, pipeline stage, and referral partner, the automation sends the wrong messages to the wrong people. A refinance nurture campaign that fires to a borrower who just closed a purchase loan damages the client relationship and wastes campaign spend. This happens constantly on self-managed deployments because nobody owns the tagging workflow at the point of entry. The platform is sound. The process breaks down before the contact even enters a sequence.

How an Aristo mortgage VA executes inside BNTouch

The VA owns contact segmentation and campaign monitoring. When a new lead enters BNTouch, the VA assigns the correct tags based on lead source and loan type, confirms the appropriate drip campaign activated, and sets a follow-up task for the broker at the right interval. For active referral partner relationships, the VA handles the co-marketing execution: building co-branded email templates with the Realtor’s information, scheduling the monthly market update campaign, and tracking open rates and click-through data so the broker knows which partners engage and which need a different approach.

The VA also runs the daily SMS compliance check, confirming opt-in status for every contact before the system sends a text and flagging any contacts who opted out so they’re suppressed correctly. That 15-minute daily task is the difference between a clean compliance record and an FCC inquiry.

Whiteboard CRM: Referral Relationship Management for Broker-Realtor Partnerships

Whiteboard CRM focuses on one thing that Total Expert and Jungo treat as secondary: the mortgage broker’s relationship with real estate agents. Its agent portal gives Realtors direct visibility into their clients’ loan status, which cuts the volume of inbound “where are we?” calls that fragment a broker’s day. The platform tracks referral source performance, measures partner engagement, and automates the touchpoints that keep agent relationships active between transactions.

Integration and compliance fit

Whiteboard integrates with Encompass and connects to email platforms, document portals, and calendar tools. Its role-based permission system allows Realtors to view file status without accessing NPI, which resolves one of the trickier access control problems in broker-agent data sharing without requiring custom configuration on your end.

The Consistency Problem: Why Whiteboard CRM Dies Without Daily Ownership

Whiteboard CRM’s value depends entirely on consistent data entry and regular communication cadences. When brokers stop updating files promptly or skip the weekly agent update emails, the Realtor portal shows stale data. Realtors stop logging in and call the broker directly instead. The tool loses its purpose the moment someone skips a week. It only works when someone owns the execution without fail.

How an Aristo mortgage VA executes inside Whiteboard CRM

The VA runs the Friday partner update: pulling the current status of every active file tied to a Realtor relationship, drafting the weekly update email with current milestones (application received, disclosure sent, appraisal ordered, clear-to-close issued), and sending it through the Whiteboard system so the full communication history stays intact. This task takes a broker roughly 90 minutes per week. The VA handles it as a standard workflow item, every Friday, without the broker touching it.

For new Realtor referral sources, the VA builds the partner profile in Whiteboard, tags the referral source on every file that came through that agent, and sets the 90-day relationship check-in reminder. When a file closes, the VA sends the post-close thank-you and updates the referral source attribution data so the quarterly referral report reflects accurate production by partner. Aristo’s remote administrative support teams running Whiteboard for broker clients manage an average of 35 active Realtor relationships per broker, a number that falls apart without a system someone runs consistently.

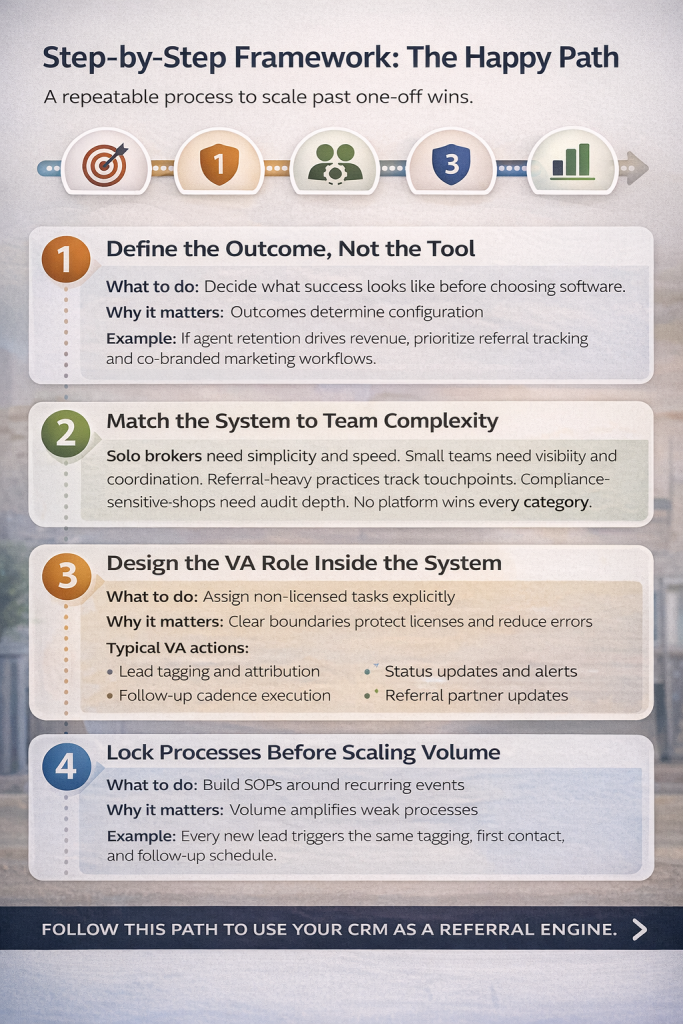

What Has to Happen Before Your VA Logs In

Dropping a VA into a CRM without a setup framework creates problems that compound fast.

Define the permission scope before anything else. Your VA’s account should reach only the records and functions tied to their specific tasks. No rate sheets, no pricing engines, no compliance disclosure workflows. Those belong to licensed users. Getting this right takes under an hour.

Write the SOPs before you delegate. A VA can’t run a task without written instructions. That means a step-by-step document covering what to do when a new lead enters, what to check during the daily pipeline review, how to handle a condition request, and what to escalate to the broker. Specific beats comprehensive. The SOP needs to be clear enough that the VA executes it without judgment calls that require a license.

SOP deployment is something Aristo handles as part of onboarding for every mortgage VA placement. The broker doesn’t start from scratch.

Set up measurement from day one. Track time to first contact on new leads, the number of outstanding conditions per file at the 10-day mark, and the percentage of files that hit clear-to-close within the contracted closing window. These three numbers tell you whether the delegation is working or stalling, and they give your VA something concrete to improve against.

The Metrics That Tell You Whether It’s Working

Pipeline reporting only matters when the numbers you track connect to outcomes. Brokers who monitor CRM logins and email open rates measure activity, not results.

The four numbers that matter: time to first contact on new purchase leads (target is under 20 minutes), active conditions per file at the 10-day mark (under three for a well-run operation), percentage of files reaching clear-to-close within the contracted window (80% or higher is the benchmark), and referral source pull-through rate by partner (which tells you which agents send qualified buyers and which generate noise).

Your VA pulls these numbers weekly from the CRM reporting module and flags anything outside the target range. The broker reviews a four-line summary. The pipeline stays in motion without daily hands-on management.

Which Platform Fits Your Operation Right Now

The right CRM depends on your biggest constraint today, not tomorrow.

A solo broker or small team moving from six to ten closings per month gets the most immediate return from BNTouch or Whiteboard CRM. Both handle lead nurture and Realtor relationship management without overwhelming a VA with excessive overhead on day one.

A multi-producer team with complex lead attribution and performance reporting needs across multiple loan officers gets more from Jungo’s Salesforce infrastructure, which scales with the data demands of a growing operation.

A team at 10-plus loans per month with multiple referral channels, Encompass as the primary LOS, and a need for enterprise-grade customer intelligence equity triggers, MIP drop-off automation, ARM adjustment alerts, rate-lock expiration workflows, fits Total Expert.

In every case, the CRM performs at the level of the person running it daily. The brokers who outperform their peers by 2:1 aren’t running better software. They’ve built a system where a trained VA owns the administrative layer and the broker stays in front of borrowers and referral partners.

Use the VA workflow calculator on this site to identify which tasks you’re currently handling that a licensed-compliant VA could own. Then book a call to build the role design for your specific CRM setup.

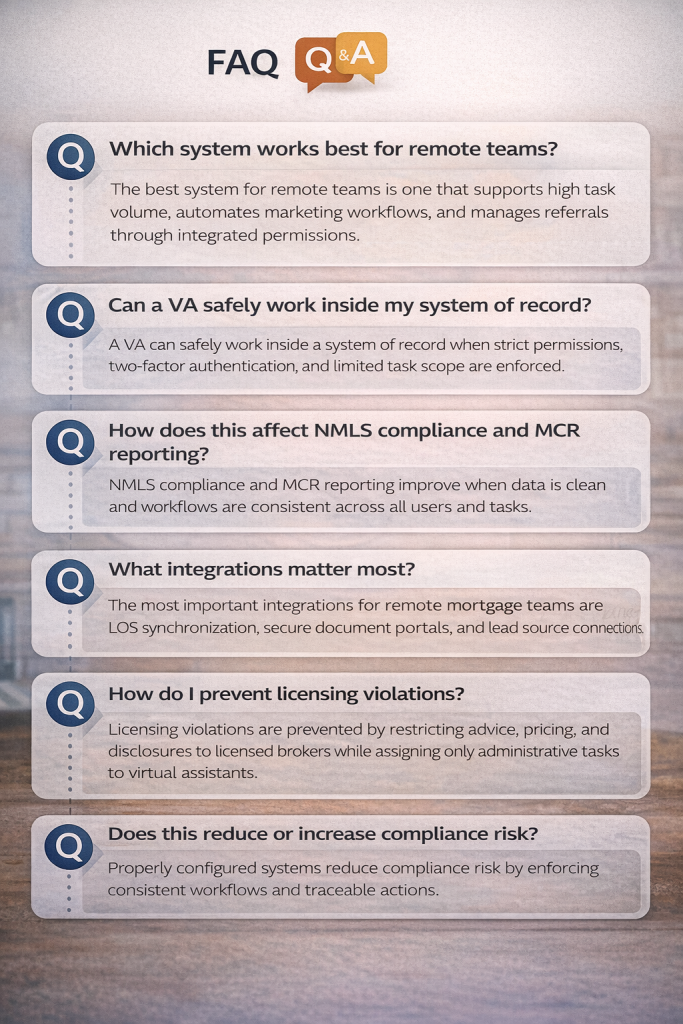

Which system works best for remote teams?

The best system for remote teams is one that supports high task volume, automates marketing workflows, and manages referrals through integrated permissions.

Can a VA safely work inside my system of record?

A VA can safely work inside a system of record when strict permissions, two‑factor authentication, and limited task scope are enforced.

How does this affect NMLS compliance and MCR reporting?

NMLS compliance and MCR reporting improve when data is clean and workflows are consistent across all users and tasks.

What integrations matter most?

The most important integrations for remote mortgage teams are LOS synchronization, secure document portals, and lead source connections.

How do I prevent licensing violations?

Licensing violations are prevented by restricting advice, pricing, and disclosures to licensed brokers while assigning only administrative tasks to virtual assistants.

Does this reduce or increase compliance risk?

Properly configured systems reduce compliance risk by enforcing consistent workflows and traceable actions.

Next Step

If you close five or more loans per month and still handle follow‑ups yourself, your system limits your growth. The fastest way forward pairs the right platform with a VA trained to run it.

Start by using the virtual assistant calculator to see how many high‑value hours you lose each week, then book a free consultation to design a VA‑ready workflow that scales without adding stress.